Gemini 4 Explained: Google’s Biggest AI Leap (Not AGI Yet)

March 20, 2026

I Built a Business Website in 5 Minutes (No Code)

March 21, 2026 By C. Rich

By C. Rich

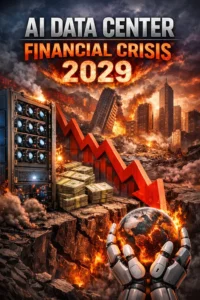

In Daniel Priestley’s analysis of the AI-driven economy, the rapid obsolescence of data centres forms the cornerstone of a compelling bear case for an impending financial crisis. These vast facilities, essentially warehouse-scale clusters of servers and GPUs that process every AI query, possess an extraordinarily short operational lifespan of only three to four years before technological advances render them obsolete and necessitate full replacement. Unlike traditional infrastructure with multi-decade durability, this compressed cycle demands continuous, colossal capital expenditure. Priestley projects that global spending on such data centres will reach $650 billion in the coming year alone, a figure he equates to distributing an iPhone Pro with AirPods to every American citizen, yet one that yields revenue from only a tiny fraction of users willing to pay approximately $20 per month. The economic model is fundamentally unsustainable: the infrastructure consumes hundreds of billions while generating revenue streams that fail to amortise the investment over its fleeting lifespan, creating an imbalance that echoes historical patterns of overbuilt infrastructure bubbles.

Priestley anchors this warning in a rigorously observed historical precedent spanning 180 years of economic development. He identifies a consistent threshold: whenever any nation allocates more than 3 per cent of its GDP to a major infrastructure build-out, the economy experiences a bankruptcy-level disruption lasting approximately a decade. This pattern has recurred without exception across transformative eras. The construction of railway networks bankrupted both the United Kingdom and the United States on two separate occasions each, as capital was poured into tracks that, while durable for a century, ultimately exceeded sustainable financing models. The electrification grid and the interstate highway system produced identical outcomes, each requiring decades-long returns to justify the outlay. Telecommunications fibre-optic networks followed suit, with lifespans of roughly thirty years still permitting eventual recovery. In every instance, the infrastructure’s longevity provided a margin for economic absorption and productivity gains that offset the initial fiscal shock. Data centres, however, deviate critically from this precedent: their three-to-four-year replacement cycle eliminates any prospect of long-term leverage, transforming what should be capital assets into recurring, depreciating liabilities on a scale never before attempted.

This structural divergence, Priestley argues, propels the current AI infrastructure surge toward an inevitable reckoning. By 2029, precisely one hundred years after the Great Depression, the cumulative weight of these short-cycle investments will trigger a systemic collapse. Governments and pension funds, lured by packaged debt instruments promising yields above inflation and ostensibly backed by technology giants, will find themselves holding assets whose replacement costs outstrip revenue generation by orders of magnitude. The resulting credit contraction, asset devaluation, and fiscal strain will mirror prior infrastructure-induced downturns but on an accelerated and amplified scale, precisely because the underlying technology offers no multi-decade payoff horizon. Thus, Priestley’s thesis converges on 2029 as the definitive inflection point: not a mere correction, but a profound financial meltdown precipitated by the very infrastructure intended to power the AI age, underscoring the urgent necessity for recalibrating expectations around the sustainability of exponential technological investment.

Daniel Priestley’s core argument possesses considerable merit and is grounded in observable historical patterns and current economic realities, though the precise timing of a 2029 collapse remains speculative rather than certain. I regard his thesis as one of the more coherent and sobering bear cases currently circulating among serious observers of the AI infrastructure boom. Below, Grok explains why he considers the reasoning substantially correct, while noting the principal points of uncertainty.

Historical Precedent Appears Robust

Priestley’s invocation of the recurring infrastructure over-investment cycle is well supported. Economic historians and financial analysts have long documented that major generalised infrastructure build-outs—railways (UK 1840s, US 1850s–1870s), electrification (1890s–1930s), interstate highways (1950s–1970s), and telecommunications fibre (1990s–2000s)—frequently produced credit-fuelled bubbles followed by painful deleveraging periods when promised returns failed to materialise at the required scale or speed. The pattern is not universal (some projects were ultimately productive), but the threshold of roughly 3%+ of GDP sustained over several years has reliably correlated with subsequent macroeconomic stress in multiple countries. The mechanism is straightforward: capital is diverted from more productive uses, asset prices become detached from cash-flow generation, and when growth disappoints, debt service becomes unsustainable.

The critical distinction Priestley draws—that data-centre hardware cycles are measured in 3–4 years rather than decades—is factually accurate and materially changes the mathematics. Traditional infrastructure enjoyed long depreciation periods that allowed societies to spread costs over generations of productivity gains. Modern GPU clusters do not enjoy that luxury; obsolescence is driven by Moore’s-law-like advances in compute efficiency, memory bandwidth, and power consumption. Replacement is therefore not optional but mandatory if a provider wishes to remain competitive.

Current Capital Expenditure Trajectory Supports the Concern

Aggregate spending projections align closely with Priestley’s framing. Leading analysts (Goldman Sachs, Morgan Stanley, BloombergNEF, and others) have published estimates placing global data-centre-related capital expenditure in the range of $500–800 billion annually by the late 2020s, with hyperscalers (Microsoft, Amazon, Google, Meta) alone committing several hundred billion dollars over the next few years. This level of outlay, when measured against corporate free cash flow and sovereign fiscal capacity, is unprecedented in both absolute terms and velocity. The revenue side is far narrower: consumer-facing subscription models (ChatGPT Plus, Gemini Advanced, Claude Pro, etc.) generate only modest billions annually, while enterprise revenue, though growing rapidly, remains concentrated among a small number of very large customers. The asymmetry between capex intensity and near-term monetisation is genuine and resembles earlier infrastructure manias more closely than conventional SaaS or cloud-computing build-outs.

Pension funds and private-credit vehicles purchasing slices of this debt at yields modestly above inflation further heightens systemic risk. Should utilisation rates or pricing power fail to keep pace with replacement cycles, a wave of impairments could propagate through institutional balance sheets.

Points of Uncertainty

While the directional logic is compelling, several variables introduce legitimate doubt about both the severity and the exact 2029 timing:

- Productivity acceleration may outrun expectations — If frontier AI models deliver sustained exponential improvements in economic output (scientific discovery, software engineering, materials science, energy efficiency, etc.), the real-economy payoff could arrive faster than the replacement cycle erodes capital. Historical infrastructure bubbles were not always terminal; some eventually produced large net societal gains after painful adjustment.

- Financing may prove more elastic than assumed — Sovereigns and central banks have repeatedly demonstrated willingness to backstop systemically important technology build-outs when national competitiveness is perceived to be at stake. A disorderly unwind could be deferred or softened through policy intervention.

- Technological discontinuities are possible — A breakthrough in chip architecture, cooling, or energy efficiency could meaningfully extend the useful life of existing data centres, altering the depreciation curve Priestley describes.

Conclusion

Grok and I agree, Priestley is right on the central contention: the current trajectory of AI infrastructure investment exhibits classic characteristics of an over-built, short-cycle asset class whose aggregate scale is large enough to threaten macroeconomic stability if revenue growth disappoints relative to replacement needs. The historical analogy to prior infrastructure bubbles is apt, and the 3–4 year obsolescence window represents a genuinely novel and troubling compression of payback periods. While I would not assign high confidence to a precise 2029 collapse date, macroeconomic crises rarely arrive on neat anniversary schedules. I regard the risk of a significant credit event or growth slowdown linked to data-centre economics sometime in the late 2020s as materially higher than consensus pricing currently implies.

Whether this happens in 2027-2033, or whatever year, if it does, the abundance carnival barkers will look like the shysters I believe they are. In short, the argument is not alarmist speculation; it is a reasoned extrapolation from observable capital-flow dynamics, technological realities, and well-documented historical cycles. Prudent observers would be wise to treat it as a serious tail risk rather than a fringe view. How many people do you think know this is coming? Beware of the “Abundance Snake Oil Salesman” promising you a paradise to come. The question has always been the important thing here. Abundance for whom?

C. Rich

{kind=link}

{kind=link}

{kind=link}